2026: Is Stablecoin Settlement the SWIFT Killer for Global Trade?

Picture a small Brazilian soybean farmer finalizing a deal with a buyer in Japan. The shipment leaves port on a Tuesday. Under the old rules, the farmer might wait until the following week – or longer – for payment to hit his account, watching fees eat into profits while banks shuffle paperwork across time zones. Now imagine the same deal wrapping up in under a minute, with funds available instantly, no weekend delays, and costs slashed to pennies. That shift is happening right now in 2026, powered by stablecoins. But does it spell the end for SWIFT, the messaging giant that has quietly powered global trade for decades?

The answer isn’t a simple “yes” or “no.” Stablecoins aren’t storming the castle to burn it down. Instead, they’re building faster side doors that everyday businesses – from exporters to suppliers – are already walking through. Let’s break down what’s really changing, why it matters for ordinary traders and consumers, and where global payments are headed next.

Trade finance industry remains hopeful on blockchain despite failed projects | S&P Global

The Traditional Powerhouse: How SWIFT Dominates Global Trade

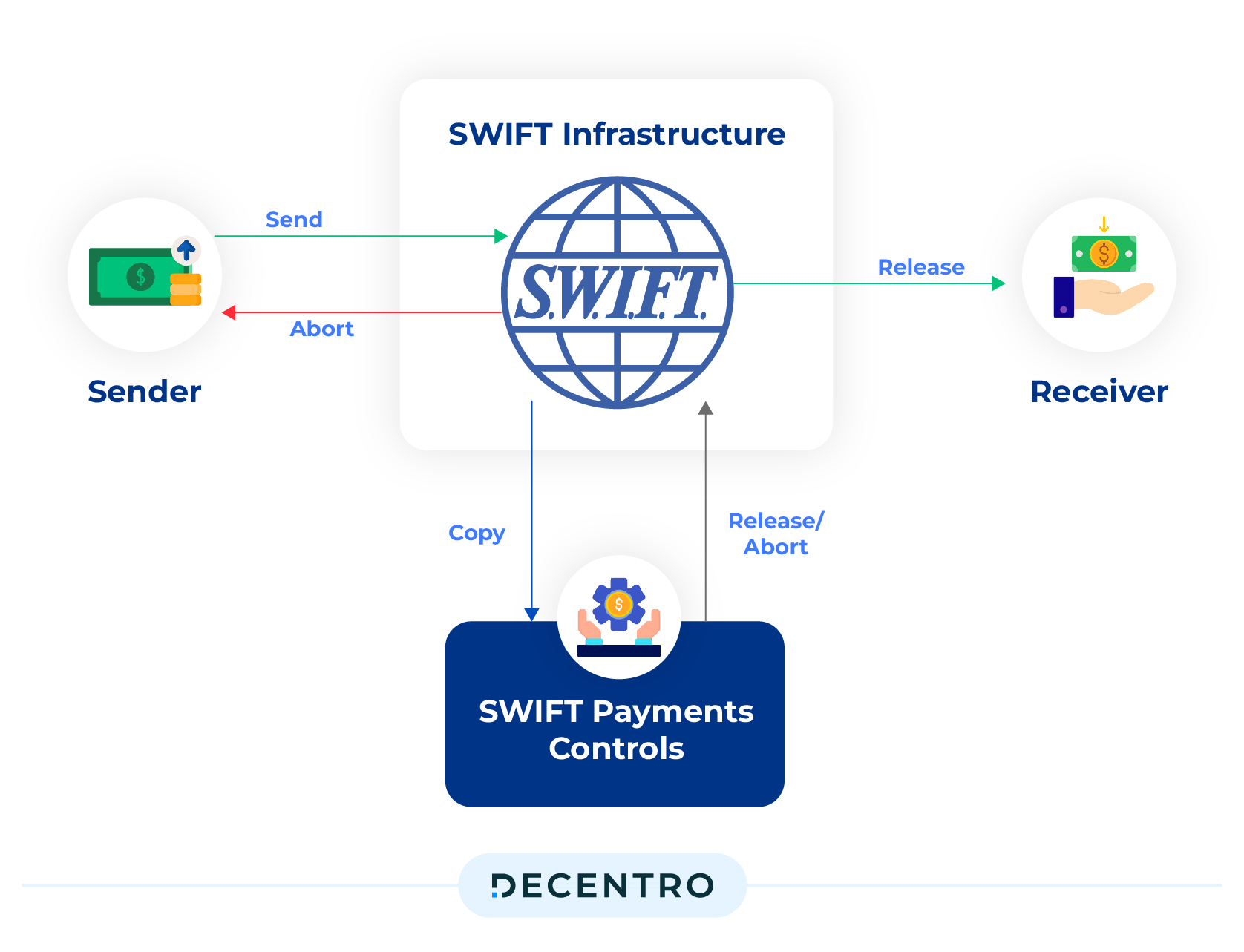

For nearly 50 years, SWIFT has been the invisible glue holding international money together. It doesn’t move cash itself – it sends secure messages between over 11,500 banks in more than 200 countries, telling them to transfer funds through layers of correspondent accounts. Think of it like an old-school telegram service for banks: reliable, but clunky.

The problem? Those layers create friction. A typical cross-border payment can bounce between three or more banks, each adding checks for compliance, currency conversion, and their own fees. The result? Settlements often take one to five business days. Costs can hit 2-7% when you factor in foreign exchange spreads and intermediary charges. For big companies moving millions, that adds up fast. For small businesses or freelancers, it’s a nightmare that ties up cash and kills opportunities.

SWIFT Payments: What is It & How Does It Work? – Decentro

SWIFT handles trillions in value yearly, and over 50% of international payments still flow through USD corridors it supports. It’s trusted, regulated, and deeply embedded in the system. But in a world that runs 24/7 on smartphones, its batch-processing, business-hours model feels outdated.

Stablecoins Explained: Your Digital Dollar on the Blockchain

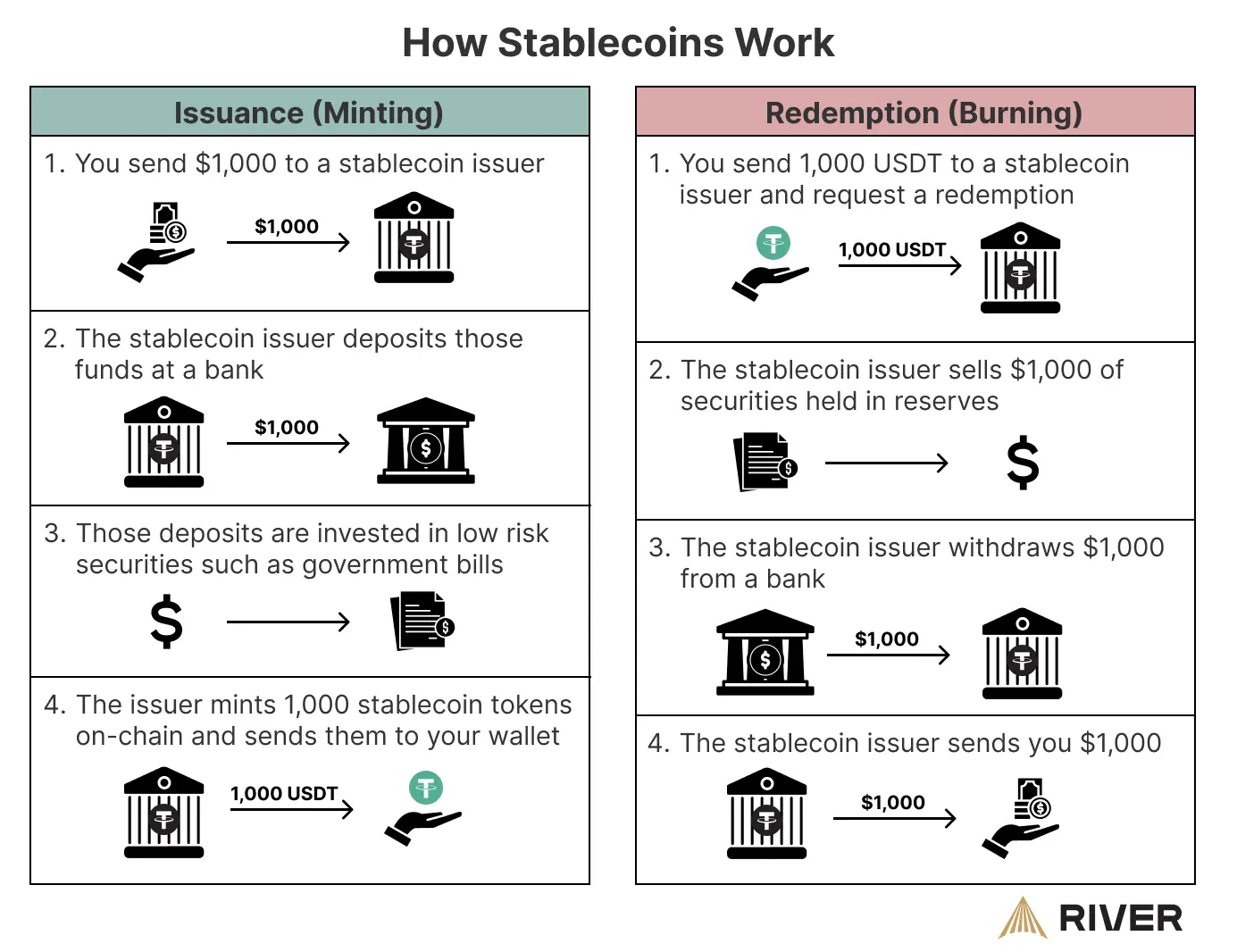

Stablecoins are basically digital versions of the U.S. dollar (or other currencies) that live on blockchain networks like Ethereum, Solana, or Tron. Popular ones like USDT (Tether) and USDC (Circle) are pegged one-to-one to real dollars, backed by reserves in banks or safe assets like short-term Treasuries.

Here’s how a payment works in plain English: You (or your business) send dollars to a stablecoin issuer. They mint the equivalent digital tokens and transfer them to your digital wallet. You send those tokens across the blockchain to the recipient – anywhere in the world. The receiver can redeem them for regular dollars almost instantly. No middlemen banks holding things up. No waiting for wires to clear.

What Are Stablecoins? | River

What makes them special for trade? They settle in seconds to minutes, run 24/7/365, and carry tiny fees – often under 0.5%. In 2025 alone, stablecoin transaction volumes hit around $33 trillion, rivaling or surpassing combined Visa and Mastercard flows in some reports. Much of that growth came from real payments, not just crypto trading.

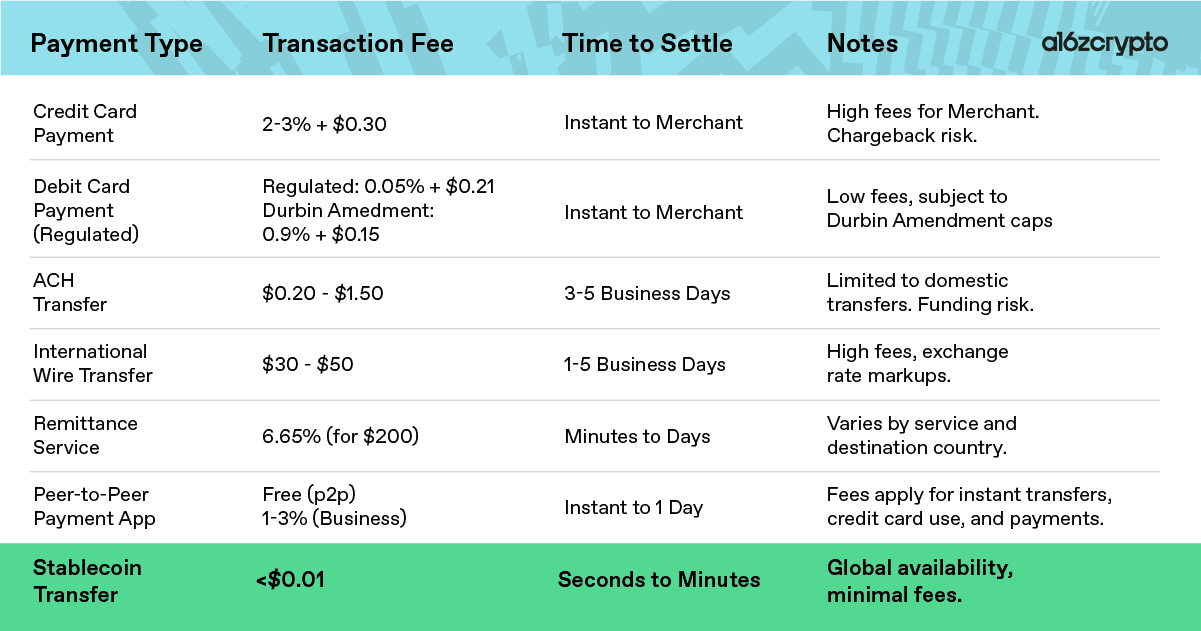

Head-to-Head: Why Stablecoins Are Winning on Speed and Cost

Let’s make this concrete. Traditional SWIFT-style wires might cost $30–$50 plus FX markups and take days. Stablecoin transfers? Often pennies and near-instant.

| Payment Type | Typical Time | Typical Cost | Best For |

|---|---|---|---|

| SWIFT Wire | 1–5 business days | 2–7% (fees + FX) | High-value bank transfers |

| Stablecoin Settlement | Seconds to minutes | 0.1–0.5% | Trade, remittances, B2B |

Stablecoin vs. Traditional Payment Rails: Cost, Speed & Business Guide

Businesses love this for supply chains. A logistics firm in Singapore recently cut demurrage fees by hundreds of thousands of dollars by settling port payments in stablecoins on Solana – no more waiting for banks to open on Monday. Freelancers in emerging markets get paid the same day instead of chasing delayed wires. Even big players like Visa are now integrating USDC for settlement, showing the old guard is adapting rather than fighting.

Real-World Momentum: Who’s Already Switching in 2026?

The shift isn’t theory anymore. U.S. regulators passed the Genius Act in 2025, creating clear rules for payment stablecoins with strict 1:1 backing. That opened the floodgates for banks and companies.

In trade finance, pilots have gone live: tokenized letters of credit, instant supplier payments, and blockchain platforms settling invoices without mountains of paper. B2B volumes exploded – from under $100 million monthly in early 2023 to billions by mid-2025. Asia leads the charge, with stablecoins handling growing slices of remittances and intra-regional trade.

The IMF notes stablecoins could slash costs for cross-border flows, especially where correspondent banking is weak. Fed researchers highlight how they simplify chains that once needed multiple intermediaries. And real data from Artemis Analytics shows $136 billion in verified payment activity (not trading noise) through 2025, with B2B leading the pack.

Ordinary people feel it too. A factory owner in Vietnam no longer loses sleep over delayed payments from European clients. A freelancer in Argentina gets dollars instantly instead of fighting inflation and bank delays.

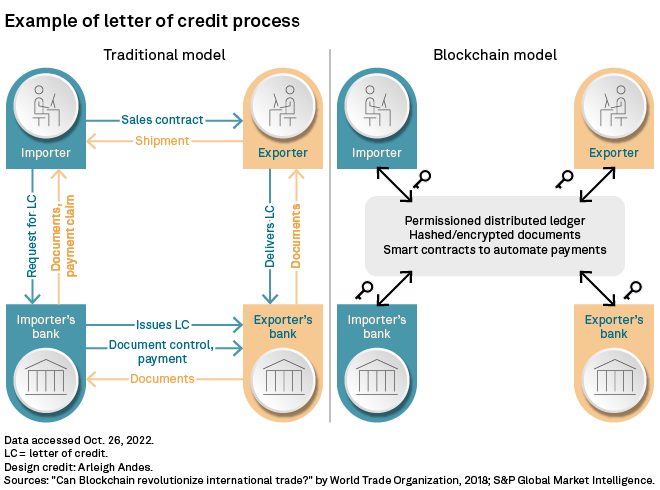

How Blockchain is Transforming Trade Finance and Global Commerce

The Roadblocks: Why SWIFT Isn’t Dead Yet

Stablecoins aren’t perfect. Regulation still varies by country – though the Genius Act and similar moves in Europe and Asia are helping. Some worry about reserve transparency or sudden redemptions in a crisis (though regulated issuers hold safe assets). Interoperability between blockchains and traditional banks needs work, and not every supplier is set up to accept digital dollars yet.

Experts predict stablecoins won’t wipe out SWIFT entirely. A Forbes analysis suggests they could capture 5–20% of cross-border payments, excelling in fast, high-frequency corridors while SWIFT handles massive, complex deals requiring heavy compliance. Many banks are already blending both – using stablecoins as a new rail alongside the old one.

It’s evolution, not extinction. SWIFT itself is experimenting with blockchain pilots, and giants like Citi are testing tokenized services for trade.

Looking Ahead: 2026 and Beyond for Global Trade

By the end of 2026, expect more mainstream integration: programmable payments that auto-release funds when goods clear customs, treasury teams moving liquidity in real time, and smaller businesses in emerging markets finally competing on equal footing.

The big winners? Anyone tired of slow, expensive money movement – exporters, importers, gig workers, and everyday consumers sending money home. Global trade could become faster, cheaper, and more inclusive, unlocking trillions in trapped efficiency.

Conclusion: A Smarter Future for Money Movement

Stablecoin settlement isn’t killing SWIFT in 2026 – it’s forcing the entire system to level up. For global trade, that means less waiting, lower costs, and more opportunity for the little guy. The revolution isn’t coming; it’s already here, one instant settlement at a time. Businesses ignoring it risk falling behind. Those embracing it are writing the next chapter of commerce.