Picture this: You send $100 to a friend using a stablecoin like USDC or Tether, and it arrives in seconds for pennies in fees. But what if that digital dollar suddenly loses its peg and crashes to 80 cents? That fear kept many everyday Americans on the sidelines of crypto. Now, the FDIC has just dropped a massive 190-page rulebook that could change everything. Approved on April 7, 2026, this proposal turns the GENIUS Act into real-world guardrails for stablecoins issued by banks and their subsidiaries. It’s not flashy headlines—it’s the boring-but-crucial fine print that could make your digital wallet feel as safe as your checking account.

Let’s walk through what this hefty document actually means for regular people, why it matters, and how it balances innovation with old-school banking safety.

FDIC Proposes New Framework for Bank-Issued Stablecoins Under Federal Regulation

What Exactly Is the GENIUS Act?

Signed into law by President Trump in July 2025, the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) was the first big federal law to bring order to stablecoins—the crypto tokens designed to hold steady at $1 each.

Before this, stablecoins operated in a gray zone. Some issuers promised safety but faced scandals when reserves didn’t match. The GENIUS Act created a clear framework: Only “permitted” issuers can create these tokens for everyday use, and they must follow strict rules on reserves, redemptions, and disclosures. The goal? Make stablecoins a trusted tool for payments, not just crypto trading.

The FDIC’s new proposal is the second piece of the puzzle. It focuses on banks under FDIC supervision—think community banks and regional players—showing exactly how they (and their subsidiaries) can issue stablecoins safely.

Breaking Down the 190-Page Rulebook: The Big Changes

This isn’t a quick memo. The FDIC’s notice of proposed rulemaking (NPRM) spans nearly 191 pages and spells out a “prudential framework” tailored to bank-backed stablecoins.

Here’s what stands out for everyday users:

- Ironclad 1:1 Reserves: Issuers must hold real, identifiable assets—like cash or short-term Treasuries—equal to every stablecoin in circulation. No mixing with other funds, and everything must be segregated. Monthly public reports keep it transparent.

- Fast Redemptions: You want your dollars back? Issuers have to redeem within two business days—no more waiting weeks or facing excuses.

- No Yield Promises: Stablecoins can’t pay interest or claim to earn you extra returns. This keeps them simple and safe, not like risky savings products.

- Capital and Risk Rules: Banks must hold extra capital and manage risks like interest-rate swings or hacks. It’s customized based on the issuer’s size—no one-size-fits-all that could crush small players.

The rule also covers custodians—banks holding reserves for stablecoin issuers—and sets standards so your assets stay protected.

Why No FDIC Insurance for Stablecoin Holders?

This is the part that might surprise people used to bank accounts. The proposal makes crystal clear: Deposits used as stablecoin reserves are not insured to the token holders on a pass-through basis.

In plain English: If the stablecoin issuer runs into trouble, you don’t get automatic FDIC protection like your checking account. Why? Stablecoins aren’t traditional deposits—they’re a new digital tool. The GENIUS Act itself says they aren’t backed by the “full faith and credit” of the U.S. government.

But here’s the silver lining: The reserves themselves sit in FDIC-insured banks, and the rules are designed to prevent runs or failures in the first place. It’s safety through strong rules, not insurance payouts.

Stablecoins Get Their Own Rulebook: Introducing the GENIUS Act of 2025

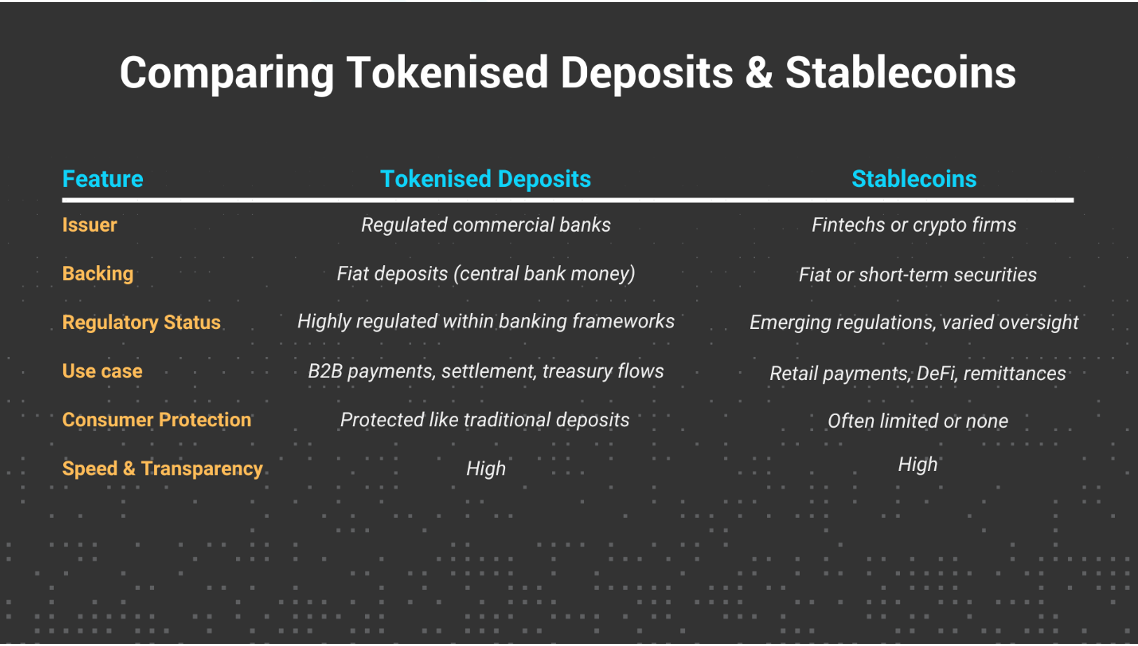

Tokenized Deposits vs. Stablecoins: The Key Distinction

The FDIC didn’t stop at stablecoins. The rulebook also clarifies tokenized deposits—basically, regular bank deposits turned into digital tokens on a blockchain.

Good news for banks experimenting with this tech: If it meets the legal definition of a “deposit,” it gets full FDIC insurance treatment, just like your regular savings.

This creates a clear split:

- Stablecoins → New digital money for payments, strict non-bank-like rules, no insurance pass-through.

- Tokenized Deposits → Bank IOUs on the blockchain, fully insured and treated like old-school money.

It’s a smart way to encourage innovation without blurring lines that could confuse consumers.

What are tokenised deposits and stablecoins? The future of digital payments explained | by Jonny Fry Editor of Digital Bytes | Medium

How This Helps Everyday People and the Economy

For regular folks, the biggest win is trust. Stablecoins already handle trillions in transactions yearly—mostly in crypto trading or cross-border payments. With these rules, they could become everyday tools: cheaper remittances for families abroad, instant business payments, or even settling your coffee tab without bank delays.

The rules also protect against the wild risks that made headlines in past crypto collapses. Strong reserves and quick redemptions mean less chance of a sudden de-pegging that wipes out your savings.

On a bigger scale, experts say this could boost demand for U.S. Treasuries (since issuers must hold them) and strengthen the dollar’s global role. It’s innovation that actually reinforces traditional finance, not fights it.

What Happens Next?

This is just a proposal. The FDIC is opening a 60-day public comment period so banks, fintechs, and everyday users can weigh in. After that, they’ll review feedback and issue a final rule.

The GENIUS Act itself takes full effect in January 2027 (or sooner once all regulators finish their pieces). Until then, the industry gets time to prepare.

Challenges remain: Some worry the rules are too strict for smaller issuers, while others fear they don’t go far enough on consumer protections. But the FDIC’s careful approach—aligning closely with the Office of the Comptroller of the Currency—shows regulators are learning from past mistakes.

The Bottom Line: Safer Stablecoins Ahead

The FDIC’s 190-page rulebook isn’t sexy reading, but it’s a landmark step toward making stablecoins boringly reliable—like cash in your pocket, but faster and borderless. By enforcing rock-solid reserves, speedy redemptions, and clear boundaries from insured deposits, it gives everyday Americans a reason to trust digital dollars.

Whether you’re a crypto newbie sending money overseas or a small business owner tired of slow wires, this could open doors to a smoother financial future. The GENIUS Act set the vision; the FDIC just handed us the practical blueprint.

What do you think—will these rules finally make stablecoins mainstream, or are they holding back innovation? Share your take in the comments.